Table of contents

When it comes to managing Roth IRAs, we believe understanding the five-year rule is essential for making informed decisions, particularly when considering Roth conversions versus direct contributions. This rule, although seemingly straightforward, we feel carries important nuances that can significantly impact your financial strategy and the accessibility of your funds.

What is the Roth IRA Five-Year Rule?

The Roth IRA five-year rule requires that five tax years must pass from the date of your first contribution to a Roth IRA before earnings can be withdrawn tax-free. This is crucial for anyone looking to leverage the tax advantages of Roth IRAs fully.1

Roth Distribution Order

When taking distributions from your Roth IRA, they are considered in this order:

- Regular contributions

- Conversions

a. Taxable portion – This would be a normal Roth conversion where it is all taxable.

b. Nontaxable portion – This would be like a non-deductible IRA conversion. - Earnings on contributions – This is worth highlighting. Imagine you’ve contributed to your Roth IRA for years; in-total, you’ve contributed $100,000 and the account is now worth $300,000, with earnings of $200,000. You then do a conversion of $150,000. The amount you’d be able to withdraw penalty free would only be your original contribution of $100,000. You would not be able to access the $200,000 of earnings since you must withdraw the conversion first, and it would not have satisfied the 5-year hold period yet.1

The Distinction Between Contributions and Conversions

Contributions: The clock starts ticking for contributions from the tax year in which you make your first deposit into the Roth IRA. These contributions can be withdrawn any time, tax- and penalty-free, and are not subject to the five-year rule.

Conversions: Each conversion has its own five-year clock. This is particularly important because it affects how soon you can access converted funds without penalties. Unlike contributions, converted amounts need to stay in the account for at least five years to avoid a 10% penalty on withdrawals, regardless of the account holder’s age.1

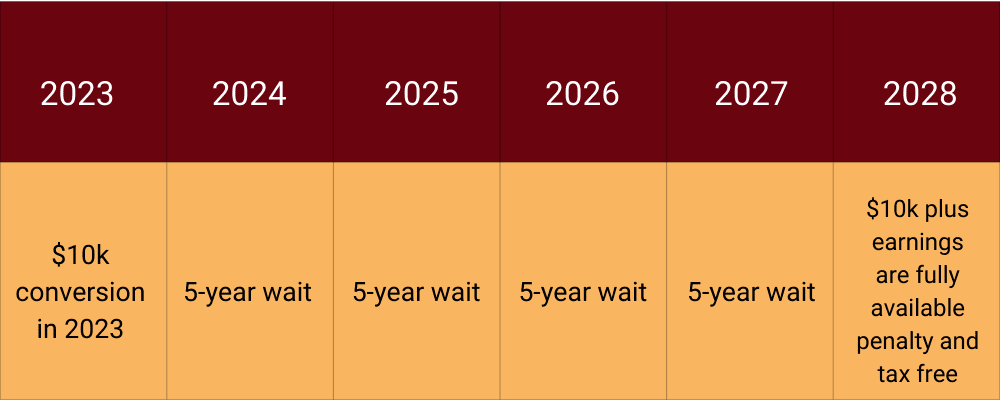

Practical Example: The Impact of Conversion Timing

Imagine converting $10,000 from a traditional IRA to a Roth IRA in 2023. According to the five-year rule, you wouldn’t be able to withdraw these funds penalty-free until January 1, 2028. Below is a visual illustrating a situation where an individual has implemented a Roth conversion strategy. Note when the converted funds are accessible and the discrepancy between the account value and the amount accessible penalty-free.1

Source: https://www.irs.gov/pub/irs-pdf/p590b.pdf

Why Timing Matters

Suppose you anticipate needing access to these funds within the next five years. In that case, converting to a Roth may not be the best strategy due to the penalty on early withdrawals from the conversion amount. Instead, if you are over age 59.5, you might instead consider opting to take a distribution and invest it in a non-qualified account, which doesn’t bind your funds under the same rules but also doesn’t offer the same tax benefits.

Starting the Clock: Contributing Early

One strategy to consider for maximizing the benefits of the Roth IRA is to start the five-year clock as early as possible. Even a minimal contribution can begin the countdown, giving you a head start on enjoying tax-free earnings on qualified withdrawals in the future.

Key Takeaways

- We believe the Five-Year Rule is crucial for planning when and how to access Roth IRA funds, especially after conversions.

- Conversions and contributions are treated differently under the rule, impacting withdrawal strategies.

- Early contributions can benefit investors by starting the five-year clock sooner, potentially aligning with your long-term financial goals.

Further Reading and Resources

For more detailed strategies on Roth IRA management, consider reading our comprehensive guide on Roth conversions and our article “When Is The Right Time For a Roth Conversion?”.

To better understand the broader implications of Roth IRAs and retirement planning, refer to the IRS’s official guidelines on Roth IRAs and a detailed analysis by Investopedia on this topic.

By keeping these points in mind, you can make more educated decisions that align with your financial needs and goals, particularly if you are considering executing complex maneuvers like Roth conversions.

Sources: https://www.irs.gov/pub/irs-pdf/p590b.pdf